MCOB - Equity Release Course

The Mortgage Conduct of Business (MCOB) for Equity Release applies to businesses that make recommendations or provide personalised information to customers on equity release products.

Equity release products refer to lifetime mortgages and home reversion plans. The main purpose of these rules is to ensure customers get suitable advice and are well informed about the nature of the service they receive.

Our MCOB for Equity Release Course explains the FCA's conduct of business rules for equity release contracts in the home finance business.

Course Specifications

Structure

Approximately 40-minute long e-learning course followed by a 10-question assessment.

Audience

Suitable for all staff - examples and interactivities designed for staff at all levels. No previous knowledge or experience is required.

Design

SHARD-compliant, responsive display on all devices, accessibility on screen readers, visual design controlled via a client style sheet.

Compatibility

All Windows, Mac OSX, iOS, Android (Flash-free for mobile compatibility). AICC and SCORM 1.2-compliant, suitable for both hosted and deployed SCORM or AICC.

Tailoring

Fully customisable on Skillcast Portal CMS.

Translation

Pre-translated versions not available, but all text content can be exported for translation into all languages.

Localisation

Based on UK legislation, but suitable for global audiences upon the removal of UK-specific references and translation as necessary.

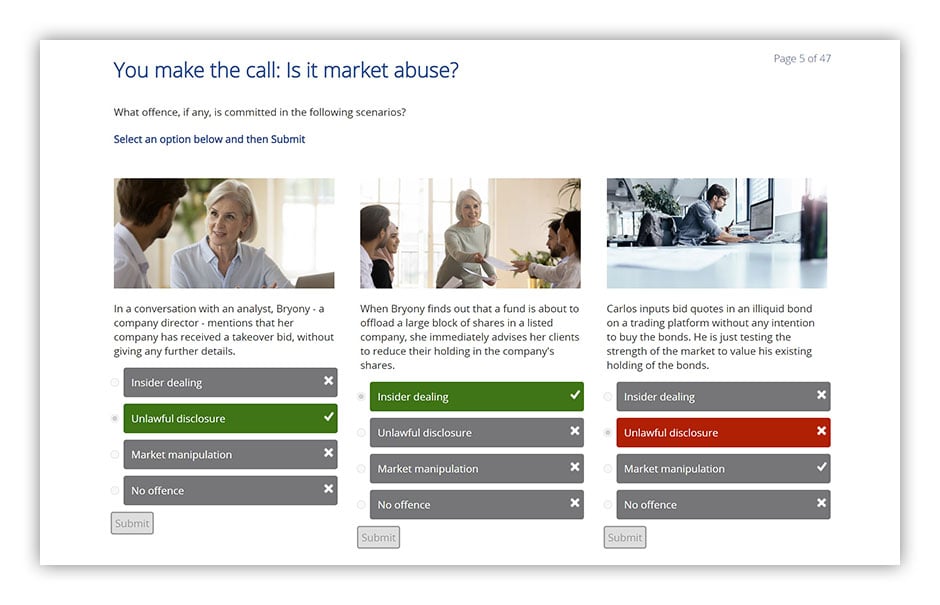

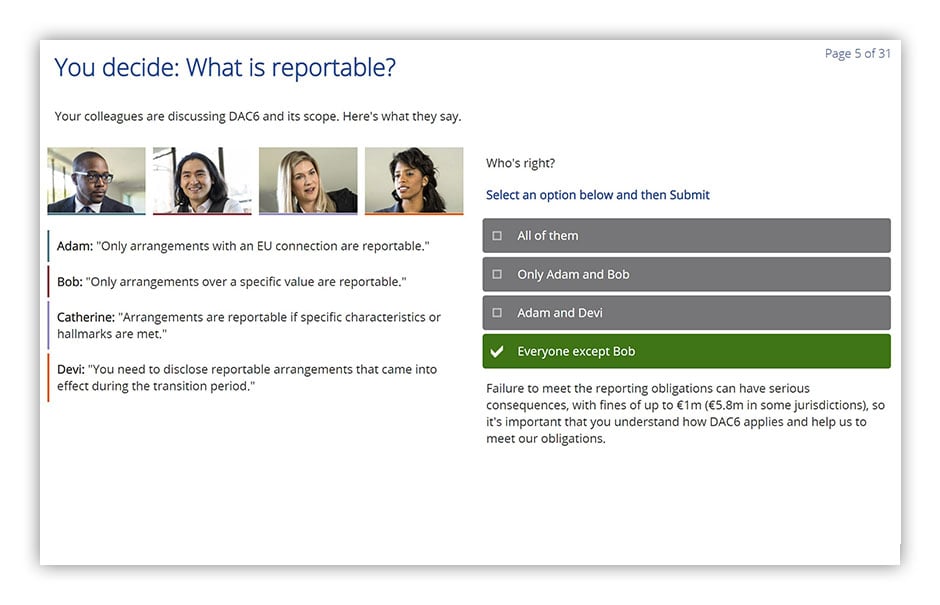

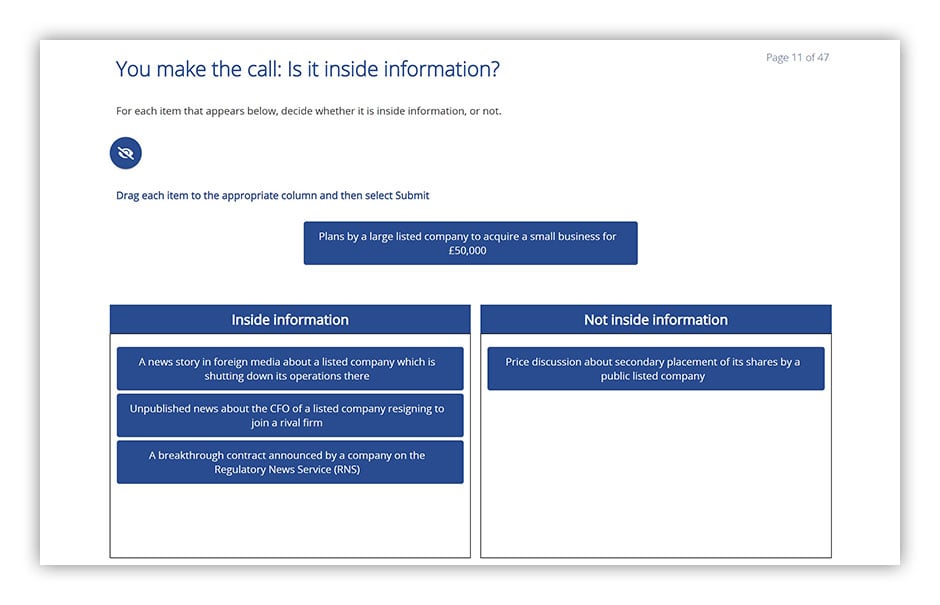

Sample Course Pages

FCA Courses Library

Our FCA Course library of over 60 training modules covers everything from high-level and conduct of business standards to thematic topics, including treating customers fairly.